What claimants actually want from redress communications

The Financial Conduct Authority’s (FCA) motor finance redress scheme is now confirmed. With 12.1 million eligible agreements in scope and implementation deadlines starting from 30th June 2026, firms handling claimant communications are under real pressure to act quickly to ensure they get it right.

But what does "getting it right" actually look like from a claimant's perspective? On 30th March, The FCA published Policy Statement 26/3: Motor Finance Redress Scheme specifically to answer that question. The findings are instructive and carry direct implications for how legal firms and lenders approach their outbound communications strategy.

The letter is far from dead

The research is unambiguous on channel preference: claimants want a letter. Across both phases of qualitative research, posted letters were consistently viewed as official, harder to fake, and more likely to be opened. Most participants said they open almost all letters, particularly those that look official or are personally addressed.

Contrast that with email. Claimants described it as higher risk and associate it with phishing, spam and scams. For those with historic motor finance agreements they may have long forgotten, an email from an unfamiliar sender is easily dismissed or deleted. As one participant put it: "I would more than likely open a letter but could mistake an email for junk."

This isn't a generational quirk. Even participants who preferred digital communication acknowledged they'd only open emails from senders they already recognised. For a redress scheme spanning agreements dating back to 2007, that's a significant problem.

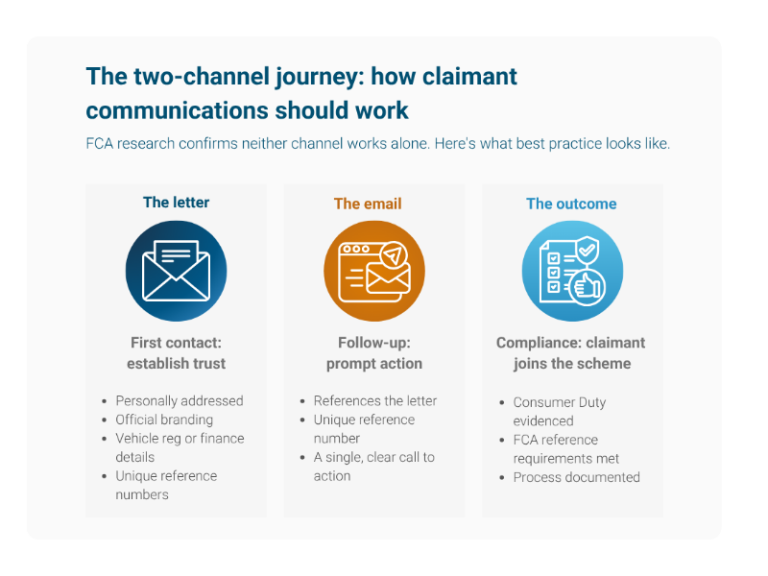

The case for channel orchestration

The strongest signal in the research isn't letter vs. email. It's both, working together. A combination of letter and email was welcomed precisely because it allowed claimants to cross-check and verify authenticity. The letter establishes legitimacy while the email drives speed and action.

This matters for Consumer Duty compliance too. PS26/3 is explicit: firms must consider customer needs, including those of vulnerable consumers, when selecting communication channels. Defaulting to email isn't a defensible position. Channel choice needs to be deliberate and evidenced.

Personalisation isn't optional

The research is equally clear on what makes communications credible: specific details. Information like vehicle registration numbers, finance terms and personal addresses. Generic communications addressed to "the owner occupier" were largely ignored.

For firms managing thousands of claimant records, many with incomplete or aged data, this creates a real operational challenge. Every outbound communication needs to be personalised, accurate and traceable because the FCA now mandates unique reference numbers in all consumer-facing scheme correspondence.

What this means in practice

The firms that will successfully navigate this scheme are those treating communications as a compliance discipline, not an afterthought. That means clean data, multichannel orchestration and the ability to generate individually personalised letters and emails at volume, all within tight regulatory timelines.

At Paragon, our redress solution is built for exactly this kind of high-stakes, high-volume environment. If you're currently working through your communications approach for the redress scheme, we'd love to speak to you.